Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

The transformation of transparency technology impacts business activities and environmental issues. The technology allows the business to embark their activities into a glo bal market, automate the business process, and enhance the business effectivity. Technology in business activities has been identified as causing environmental problems by addressing environmental degradation, climate change, food scarcity, pollution, and waste problems (Martinez, Rambaud, &Oller, 2019). Business society tends to adopt technology to reduce expenses and impro ve their business efficiency, which puts society and the environment at risk. The demand for companies to provide information on environmental protection and societal empowerment has increased significantly (Chakrabarty & Wang, 2012). This report is reflected in Corporate Social Responsibility (CSR) disclosure.

Disclosing non-financial reports pro vides financial and non-financial benefits to companies and society. CSR disclosure benefitted the company by reducing asymmetric information between the company and its stakeholders, lifting the company’s reputation, and reducing risk (Nekhili, Nagati, Chtioui, & Rebolledo, 2017). The strategic decision to report voluntary disclosure is essential to obtaining societal legitimacy and reducing the risk (Elfeky, 2017) to gain the company’s sustainability (Wang, Li, & Qi, 2020). However, the disclosure is believed to be derived from internal and external motivations, such as meeting the legal mandate, pressure from stakeholders, and top management commitment (Dixit, Verma, & Priya, 2022), and corporate governance plays a vital role in determining the success of the implementation and the disclosure (Aboud & Yang, 2022; Stuebs & Sun, 2015) with the Board of Directors (BoD) is being the crucial tools (Endo, 2020).

The executive board is the leading actor in determining the strategic CSR implementation, and their decision leads to success. In contrast, the Supervisory Boards (SB), which have an indirect link to business decision-making by providing advice and monitoring to the executives, tend to have various contributions. As an important corporate governance tool to monitor the pe formance of BoD, SB is believed to reduce the asymmetric information between princi ple and agents and diminish the conflict bet- ween both parties, as stated in the agency theory (Matinheikki, Kauppi, Brandon-Jones, & van Raaij, 2022). This board influences the executive’s decisions in main business activities and reporting and ensures that the decisions do not violate the principles (Steens, de Bont, & Roozen, 2020). The awareness of reporting CSR for the SB drives their perspectives to advise the executive to conduct and report more on their green and social activities. Although the executive’s responsiveness is the key (Shayan et al., 2022), support and advice from SB are believed to contribute significantly.

The executive board has been identified as vital for determining CSR activities (Kiliç, Kuzey, & Uyar, 2015), whereas SB contribution is still being debated. A board with a higher proportion of Independent Directors (ID) tends to have higher environmental and social performance since they assist the executive in disclosing certain information (Hussain, Rigoni, and Orij 2016). However, their significance is less significant than that of the executive (Purbawangsa, Soli-mun, Fernandes, & Mangesti Rahayu, 2020). The proportion of Non-Executive Directors (NED) on the board significantly contributes to information disclosure (Barako & Brown,2008), and Outside Directors (ODs) when significantly contribute to environmental performance (Endo, 2020). However, support specialist ODs who are experts in diver- se fields such as law, public relations, and insurance bring more influence to the disclosure than business expert ODs who have business experiences, knowledge, and advice in strategic decision-making and internal concern (Ramón-Llorens, García-Meca, & Pucheta-Martínez, 2019). The IDs have been identified as having a significant negative link to the CSR disclosure, especially on Eu ropean companies’ environmental, employee, social product and service, and supply chain topics. In contrast, the link positively influences community engagement (Adel, Hussain, Mohamed, & Basuony, 2019).

The research determines the role of SB in the company’s CSR activities, and disclosure has been intensely conducted with di fferent and inconsistent results. The variety of measurements, location, and CG system are the causes of the debate. Since the roles are still diverse, it is crucial to find a common thread from previous research on how the statistical results of these roles relate to the CSR actions to mitigate the conflicting fin- dings. A Meta-Analysis is conducted to integrate and draw a conclusion on how SB with all highlights (BI, NED, OD) affects CSR acti vities. Meta-analysis is one of the research methods used to assess the behavior of pre vious organizations using statistical results from research (Majumder, Akter, & Li, 2017). This study conducted research using several SB terms used in both corporate governance systems, one-tier and two-tier systems, and several terminologies in CSR, which may significantly affect gaining conclusion.

Based on the conflict and a desire to quantitatively synthesize the inconclusive findings, this study is conducted by set- ting three research questions based on the highlights of SB: (i) Does BI influence CSR performance? (ii) Does the NED influence CSR performance? (iii) Does the OD influence the CSR performance? This study addresses these research questions using a quantitative meta-analysis approach and a database of 39 works of literature collected from 1976- 2021. The period of the analysis is selected after Jensen and Mckling created the Agency Theory since this theory became the pioneer in describing the existence of asymmetric in- formation between principal and agent, and the presence of corporate governance be- came a vital decision to reduce the conflict (Alduais, Almasria, & Airout, 2022).

This study adopted the Hunter-Schmidt (HS) meta-analytic technique to assimilate findings across various studies for two reasons described by (Bhatia & Gulati, 2021). First, it does not make any assumptions about how the sample studies are distributed. Then, compared to the other estimators such as Hedges-Olkis (HO), DesSimonian and Laird (DL), and Restricted Maximum Likelihood (REML) approaches, the HS estimators show a lower mean squared error. By far, our study is the first to quantitatively aggregate the result of SB on CSR activities using meta-analysis. This research explores the effect of SB using three highlights on CSR performance to analyze the consistency of the previous findings. This study also gathered the terminologies of CSR. Therefore, this study offers a comprehensive quantitative approach to finding the role of SB in the company’s CSR activities.

Literature Review

Previous studies provided different perspe tives explaining the role of SB on CSR disclosure, and five (5) theories were identified as basis standpoints: agency theory, stakeholders’ theory, institutional theory, legitimacy theory, and resource dependency theory. The majority have confirmed the agency theory as a fundamental paradigm for how corporate governance affects the form of CSR; Jensen & Meckling (1976) state that an agency relationship is a contract between a manager (agent) and an investor (principal). The separation between the ownership and control functions in agency relations causes agency problems and conflicts. As the stra tegic decision maker, the agent potentially makes decisions that suffer the principal’s wealth. Corporate governance is a way to reduce the conflict due to asymmetric in- formation by providing monitoring activities to supervise the directors’ actions, which lie in the company’s structure (Alduais et al., 2022). The principal can also limit the divergence of its interests by providing a decent level of incentive to the agent and is willing to incur supervision costs to prevent fraud committed by the agent. Agency theory see ks to explain the most efficient determination of contracts that can limit conflicts or agency problems. Conducting CSR is an activity that creates conflict between both parties, leading to additional costs that potentially reduce the profit (Shayan et al., 2022) and is believed only to improve the reputation without any economic improvement (Shu, Chen, Lin, & Chen, 2018). On the other hand, CSR is proven to improve long-term econo mic performance and must be conducted and reported in several countries. Therefore, the effectiveness in improving the impacts in all sectors and determining the actions are crucial, and the existence of SB to moni tor the executive is vital.

Haniffa and Cooke (2005) stated that from an agency theory perspective, the BI is more effective and objective in calculating managers’ performance than the Board of Directors. The role of BI in monitoring and providing advice to the executive helps reduce conflicts of interest between managers and shareholders (Majumder et al., 2017). BI also tends to pursue long-term value practices such as sustainability reporting (Cheng & Courtenay, 2006; Ibrahim, Howard, Angelidis, Ibrahim, & Howard, 2015) and positively affect corporate disclosure (Adel et al.,2019; Cheng & Courtenay, 2006; Donnelly & Mulcahy, 2008; Jizi, Salama, Dixon, & Stratling 2014 ; Leung & Horwitz, 2004; Majumder et al., 2017). However, other studies have shown negative or insignificant influences of this variable and proved that agency theory is not always supported. Barako et al. (2006) found that companies with a high level of BI have a lower need to rely on corporate re- porting to convince their stakeholders of the legitimacy of their operations. The high number of BI, more than half of the total directors, showed a lack of association with the sustainability report since they are not in- volved in daily operations in the Asia-Pacific corporations (Amran, Lee, & Selvaraj, 2014).

Different perspectives have been shown by the stakeholders’ theory regarding CSR activities. Stakeholder theory (Freeman,1999) broadly provides the basis that an organization has relationships with its internal organization but also with external parties of its organization (individuals or groups) (Francis, Hasan, Song, & Waisman, 2013). Stake- holders are groups or individuals that can be identified and can influence the achievement of organizational goals or who are in fluenced by the achievement of organizational goals (Freeman, 1999). The company’s responsibility improves the wealth of the principles and the stakeholders affected by its business activities, and CSR is a way to conduct their responsibility to the stakeholders (Torelli, 2021).

Besides the company’s function to consider the actions of the stakeholders, separating external conformity from core policies through symbolic responses allows managers to gain external legitimacy while maintaining internal flexibility (Meyer & Rowan, 1977). Managers seek to conform to socially approved norms to gain legitimacy but face pressure to maintain internal efficiency. Since society seeks corporations to be responsible for the effect of business activities on the environment and society, conducting CSR is vital to gaining legitimacy and maintaining sustainability (Cullinan, Mahoney, & Roush, 2016; David, Bloom, & Hillman, 2007; Galbreath, 2010). From the legitimacy theory and resource dependency theory perspectives, stakeholders are more accepting and more likely to supply the orga nization with the desired resources, such as capital, labor, and customers. Effective communication channels, such as sustainability reports, can influence stakeholder reactions (Dyllick & Hockerts, 2002; Wheeler & Elkington, 2001), which affect stakeholder perceptions and legitimize the organization’s existence (Hedberd & Malmborg, 2003). This increased reputation is a source of market profit and an incomparable valuable resource (Russo & Fouts, 1997). The disclosure of higher-quality information assists its stakeholders in making informed decisions- furthermore, information related to how the company’s CSR affects the role of CG in it.

CSR reporting reduces information asymmetry between managers, investors, and other stakeholders; comprehensive CSR reporting helps with manager supervision and control. Therefore, an effective board of directors is expected to promote CSR re- porting (Safieddine, Jamali, & Noureddine, 2009) if the company engages in CSR and reporting activities not only as a temporary mode but also to calm the manager’s moral problems (Hennigfeld, Pohl, & Tolhurst, 2012; (Porter & Kramer, 2006). Engaged with CSR to acknowledge the community’s concerns and maintain positive relationships with key stakeholders to improve business continuity. Companies with more effective board structures would diligently provide information on CSR-related issues.

BoD makes a strategic decision by providing a top-level decision in determining the level and types of CSR activities in a firm, including disclosure. Their actions and decisions should be determined to increase the wealth of shareholders and stakeholders. Therefore, the role of the supervisor in moni toring their decision is critical. Even though the SB should not participate in making operational decisions, their role is to ensure that the company implements CSR, supervise the company’s activities, determine the company’s strategy, and appoint and super- vise the Board of directors, which role can affect the company’s performance (Pletzer, Nikolova, Kedzior, & Voelpel, 2015).

CSR is a corporate mechanism that integrates its attention to the social en vironment into its operations. Nowadays, the company’s activities impact not only the company’s internal environment but also the external environment. Whether the company’s existence can create jobs for local communities or not, the company should care about the surrounding environment by not disposing of waste or emissions that are harmful to the environment (Aras & Crowther, 2008). CSR activities can also be defined as ethical and moral aspects of a company’s decision-making and behavior and thus address complex issues such as environmental protection, human resource management, health and safety in the work- place, local community relations, and relationships with suppliers and customers. CSR activities carried out by the company not only increase stakeholder satisfaction but also positively affect the company’s reputa tion and can reduce the occurrence of finan cial risk in the company (Gras-Gil, Palacios Manzano, & Hernández Fernández, 2016).

Several previous studies examined how SB impacts companies’ CSR performance from various perspectives. BI can in- crease corporate accountability by focusing more on the company’s and its stakeholders’ long-term interests, including social and environmental aspects (Cheng & Courtenay, 2006; Ibrahim et al., 2015). The existence of BI members improves oversight and transparency of company decisions related to CSR (Adel et al., 2019; Allegrini & Greco, 2013; Amran et al., 2014). Additionally, BI frequently pursues long-term value strategies such as sustainability reporting and has a favorable impact on business disclosure (Adel et al.,2019; Agyei-Mensah, 2016; Alipour, Ghanbari, Jamshidinavid, & Taherabadi, 2019; Biswas, Mansi, & Pandey, 2018; García-Sánchez, Hus-sain, Khan, & Martínez-Ferrero, 2021).

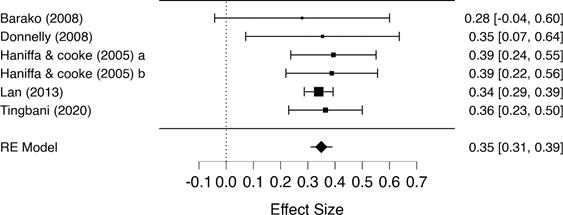

Besides BI, the role of NED as one of SB has been believed to contribute significantly to CSR performance. NED can be interpreted as members of the Board of Di- rectors who do not have executive positions in the company. NED is not involved in ma- king day-to-day operational decisions. NED generally brings independent perspectives and diverse experiences to the Board of di- rectors. NED can act as an independent supervisor and oversee the implementation of CSR within the company. The existence of NED, which has broader interests, encourages companies to pay attention to social and environmental aspects in making business decisions (Barako & Brown, 2008; Donnelly & Mulcahy, 2008; Haniffa & Cooke, 2005; Lan, Wang, & Zhang, 2013; Tingbani, Chithambo, Tauringana, & Papanikolaou, 2020).

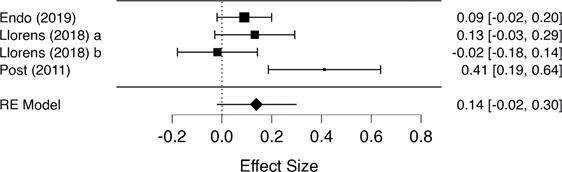

As part of the SB, an Outside Director (OD) can be interpreted as a member of the BoD who comes from a background outside the company, either from a different indus try or has experience in a different business environment (Endo, 2020). OD brings diverse and independent perspectives to the board of directors. The presence of OD who come from different backgrounds can bring broader perspectives and knowledge on relevant social and environmental issues. This perspective and experience can help identify and understand business decisions’ social and environmental impacts and encourage companies to adopt more socially responsible practices (Endo, 2020). The higher propor tion of OD is associated with more favorable CSR disclosure and a higher Kinder Lyden- berg Domini (KDL) score (Post, Rahman, & Rubow, 2011). OD tends to be more independent in making decisions, regardless of internal influences or interests in the company (Ramón-Llrens et al., 2019).

However, the results differ from (Amran et al., 2014; Barako et al., 2006; Cancela, Neves, Rodrigues, & Gomes Dias, 2020; García-Sánchez et al., 2021; Said, Zainuddin, & Haron, 2009). Given that they are not in- volved in the day-to-day operations of Asia- Pacific firms, a significant percentage of BI more than half of the total- showed a lack of association with the sustainability report (Amran et al., 2014). Companies with a high degree of BI are less likely to use corporate reporting to persuade their stakeholders that their business is legitimate (Barako et al., 2006).

The results that have not been consistent from previous studies are interesting for further research using meta-analysis to produce the following research hypotheses:

H1 |

Board Independence has a significant influence on corporate social responsibility |

H2 |

Non-Executive Director has a significant influence on corporate social responsibility |

H3 |

Outside Director has a significant influence on corporate social responsibility |

Material and Methods

This research is a systematic literature review (SLR) with a meta-analysis method that analy zes previous studies and integrates all findings on CSR and the role of board independence. SLR is a systematic way to collect, evaluate, integrate, and present findings from previous research studies that correspond to research questions (Hedges & Olkin, 1986; Retnawati, Apino, E., Djidu, & Anazifa, 2018). Meta-analysis is the statistical approach to synthesizing quantitative research results in SLR (Retnawati et al., 2018). The research process for this study was constructed into three steps and followed Schmidt’s (2015) meta-analysis procedures. Firstly, an SLR is conducted, followed by a screening and coding process. Secondly, the effect size was calculated, and the results were discussed. The detail of the procedures is described below:

SLR is Conducted by doing Literature Screening and Coding Processes

The data is collected from the biggest publishers, Emerald, Wiley, Elsevier, Sage Publishing, Springers Tailor, and Francis, from 1976, when the agency theory was created, to 2022. The selection of articles is based on the keywords “Corporate Governance,” “Board of Commissioner,” “Outside Directors,” “Independence Directors,” “Non-Executive Directors,” “Inde pendence Board,” “Corporate Social Responsi bility,” “Environmental Policy,” “Corporate Social Performance.” The keywords are created and related to the verbs that might be used in the corporate governance and CSR topic. The term in corporate governance is narrowed down to the supervisory boards. Therefore, the Board of directors and executive directors were excluded from the study. 261 papers were identified and processed into the following steps using the inclusion step, selecting articles that satisfied the criteria:

(i) having relevant topics, (ii) English language, and (iii) papers were not conference papers and working papers. In the meta-analysis, the inclusion step is selecting studies for the analysis. The inclusion step aims to select relevant studies that meet the inclusion criteria specified in the meta-analysis.

Based on the inclusion step, 101 articles satisfied the criteria. They put the next step, selecting the papers based on the exclusion criteria: (i) having a quantitative ap proach and (ii) converting the results into correlation. Based on this step, 39 articles satisfied the criteria and were analyzed.

Calculating the Effect Size

This study follows the meta-analysis procedures conducted by Schmidt (2015) and the strategy undertaken by Bhatia and Gulati (2021). The analysis begins with data extrac tion by calculating the effect size, including finding variance (Vz) and standard error ef fect size (SEz), testing the heterogeneity, and calculating the summary effect by creating a forest plot using JASP software ver sion 0.14.1 of 2020. Then, the random effect model is adopted to synthesize the empirical findings quantitatively.

This study investigates supervisory boards’ role in implementing CSR across countries. The studied countries were Japan, Malaysia, China, Australia, Taiwan, New Zealand, Indonesia, the Philippines, Singapore, Thailand, and other multi-country countries. The SB is measured through BI, NED, and OD. In contrast, CSR is measured through CSR Disclosure Index, CSR Score, Voluntary Dis- closure, Sustainability Report Credibility, Environmental Disclosure Quality, Social Score, Corporate Sustainability, and Assurance. The following table summarises previous studies used to measure research variables

Analysis and Results

Step 1 - Calculating Effect Size and the Standard Error

Effect size is a number that reflects the mag nitude of the relationship between two varia bles (Borenstein et al., 2009). After determining the sample size based on the exclusion criteria, those 39 articles were identified their coefficient correlation (r) and transformed into a Fisher index (z) as effect size andmthe standard errors (SEz) (Borenstein et al.,2009; Bosch & Card, 2012; Retnawati et al., 2018) with the formula:

The following is a presentation (r) and their transformation to Fisher (z) as an Effect Size (ES), along with the Standard error effect size (SEz) of the sample. The Standard Error of Effect Size (SEz) is used in the meta-analy- sis to estimate the accuracy or precision of each study’s calculated effect size. SEz is usually used in meta-analyses that use a correlation-based effect size, such as the Pearson correlation coefficient or the pro- duct-moment correlation coefficient (Sch-midt, 2015). ES is a statistical measure used in meta-analysis to describe the magnitude of the effect or difference between two or more groups or conditions being compared. ES provides information about the strength or magnitude of the effect observed in the studies included in the meta-analysis (Ret-nawati et al., 2018; Schmidt, 2015)

Step 2 - Heterogeneity Q-Test

After calculating the ES value and their stan dard error, the Heterogeneity test is conduc ted to ascertain and detect whether there is a publication bias in this meta-analysis study and to test whether the ES of each study used in the correlation meta-analysis is the same or different using Egger’s test (p) and Fail-Safe (N) (Schmidt, 2015). The publication bias is a problem in the meta-analysis method since this method uses previous stu- dies with significant results and non-significant results, and the possibility of publishing the significant results is higher than the non- significant ones in the systematic literature review (Borenstein et al., 2009 Rosenthal,1979). The regression based on Egger’s test is conducted to test the link between the ES against their standard errors with the null hypothesis that there is a non-asymmetric funnel plot related to the publication bias (p-value>0.05) (Schmidt, 2015). Furthermore, the Fail-safe test (N) was conducted to solve the publication bias since the research that has insignificant results has less chance of being published (file drawer), so an additional test should be included (Rosenthal, 1979). The N exceeds the critical value (5n+10), the file drawer problem is not a serious concern, and the publication bias does not exist (Bhatia & Gulati, 2021). Based on Egger’s test in Table 4, the p-value of all hypotheses is abo- ve 0.05, indicating that the null hypothesis was rejected and no publication bias has been found. This finding is supported by the Fail-safe test, which shows that the N-values are above the critical value.

Step 2 - Trim and Fill Test

This test is selected to the effect size’s bias and reduce the variance in the meta-analy sis (Duval & Tweedie, 2000; Retnawati et al., >2018). Two techniques were undertaken, first calculating the Summery effect for the random effect model to find out the number of potential studies that are missing because of publication bias and followed by perfor ming the forest plot, which portrays the presence or absence of bias from the samples (Bhatia & Gulati, 2021; Heri Retnawati et al., 2018). The estimated summary effect (rRE) indicates the level of correlation between variables, whether the correlation has a weak category (rRE 0.10), moderate (rRE= 0.25), or strong (rRE 0.40) (Cohen, Krishnamoorthy, & Wright, 2016; Retnawati et al., 2018). Then, the forest plot was tested to observe the effect size of each indicator (Figure 3).

From the first forest plot, it can be observed that the size effect of BI on CSR studies analyzed varied in magnitude between 0.01 and 0.40. From the second forest plot, the size effect of the effect of NED on CSR studies analyzed varied in magnitude between 0.28 and 0.39; and from the third forest plot, it can be observed that the size effect of OD on CSR studies varied in magnitude between -0.02 and 0.41.

Table 3 shows the results of the analysis using the Random Effects model, showing that there is a significant positive correlation between BI and CSR (z=7.385; p= <0.01; 95% CI [0.121; 0.209]). Also, there is a significant positive correlation between NED and CSR (z=15.467; p= < 0.01; 95% CI [-0.305; 0.394]). Meanwhile, the Random Effect shows no significant correlation bet- ween OD and CSR (z=1.723; p= 0.085; 95% CI [-0.019; 0.295]).

Discussion and Conclusions

This section provides a detailed discussion of the results of the meta-analysis on the link between SB and CSR by focusing on the random effect model of an association bet ween each indicator.

Meta-Analysis of BI and CSR

The results of the H1 analysis with the Random Effect model showed that there was a significant positive correlation between BI and CSR (z = 7.385; p = < 0.01; 95% CI [0.121;0.209]). This finding validates the agency theory that since asymmetric information exists between the principal and agent, which leads to agency conflict, the existen ce of IB is crucial to monitoring the actions of directors (Agyei-Mensah, 2016; Alipouret al., 2019; Biswas et al., 2018). Besides the role of advisers, BI tends to pursue the companies’ long-term practices to obtain sustainability, and providing CSR reports is essential to make it real (Cheng & Courtenay, 2006; Ibrahim et al., 1995). Since the stakeholders require companies to be more concerned about society and protect the environment, conducting CSR is a vital way to fulfill the request and gain legitimacy (Cullinan, Mahoney, & Roush, 2016; David, Bloom, & Hillman, 2007; Galbreath, 2010). IB tends to encourage the executive to con- sider the stakeholder’s needs and follow the regulations related to the society and environments to not only reduce the conflict (Alipour et al., 2019) and build the reputation (Beji et al., 2020) but also to keep the sus tainability (Hussain et al., 2018). IB strengthens the Board’s monitoring function so that companies become more responsive to re- quests for information from stakeholders (Agyei-Mensah, 2016), and the Environmen tal Disclosure Quality (EDQ) leads to better performance in companies with more inde pendent boards (Alipour et al., 2019).

Furthermore, the rejection of the null hypothesis of the Q-test (214.429) and N-test (Nfs = 3920 > critical value of 155) indi- cates the variation across the studies, andthere is no publication bias. Based on the forest plot on the trim and fill test, the correlation between IB and CSR is considered moderate (rRE=0.165). This conclusive evidence illustrates that IB’s influence on CSR implementation is positively significant.

Meta-Analysis of NED and CSR

The results of the H2 analysis with the Ran dom Effect model showed that there was a significant positive correlation between NED and CSR (z = 15.467; p = < 0.01; 95% CI [0.305; 0.394]). This finding supports the theories, including the stakeholder theory and legitimacy theory. NED is a group of di- rectors who are not involved in daily activities or making strategic business decisions but provide expert supervision and advice to exe cutives related to making decisions (Barako & Brown, 2008; Donnelly & Mulcahy, 2008). Although the executive takes the implementation of CSR, the existence of NED is proven significantly by encouraging the executive to disclose a large amount of information to outside investors (Lan et al., 2013). Effective communication with the investors and other stakeholders affects their perceptions, legitimizes the company’s existence (Hedberd & Malmborg, 2003), and increases its reputation (Russo & Fouts, 1997). Disclosing finan cial and non-financial reports is an effective communication channel (Dyllick & Hockerts, 2002). The ratio of NED on the Board is posi tively related to the breadth of information disclosed (Barako & Brown, 2008).

Moreover, after conducting the Q-test and N-test to capture a potential publication bias, the null hypothesis is rejected with a Q- test value of 0.870 and an N-value above the critical value (Nfs = 361 > critical value of 40).

The literature in this study varies, and no publication bias is present. Based on the forest plot on the trim and fill test, the correlation between NED and CSR is considered mode- rate (rRE=0.349). This conclusive evidence illustrates that the influence of NED on the implementation of CSR is positively significant. It is consistent with the arguments of Barako and Brown (2008); Donnelly and Mulcahy (2008); Haniffa and Cooke (2005); Lan, Wang, and Zhang (2013); Tingbani et al. (2020), who found that the role of NED in the corporate governance system significantly influences the actions on society and environments by mo nitoring and encouraging the executive to dis- close more information to the stakeholders.

Meta-Analysis of OD and CSR

The results of the H3 analysis with the Random Effect model showed no significant correlation between OD and CSR (z = 1.723; p = 0.085; 95% CI [0.305; 0.394]). This finding does not support the theories and fails to prove that the existence of OD tends to enhance non-financial disclosure. OD is one of the non-executive directors hired to provide an expert opinion on their expertise. Not all OD is equally effective in improving CSR dis- closure, but OD with support specialists will enhance the report (Ramón-Llorens et al., 2019). ODs from professional specialists in diverse fields, such as law, capital markets, insurance, etc., provide more benefit in en couraging the CEO to conduct and report CSR than OBs with business experts. However, this study does not support the findings of Post et al. (2011), who found that companies with a higher proportion of OD are associated with a more favorable CSR score.

Based on the Q-test and N-test, the null hypothesis is rejected with a Q-test value of

9.532 and an N-value above the critical value (Nfs = 33 > critical value of 30), indicating that the literature in this study is considered varies and has no publication bias. Based on the forest plot on the trim and fill test, the corre lation between OD and CSR is considered moderate (rRE=0.138). This conclusive evidence illustrates that OD’s influence on CSR imple mentation is positively significant.

Using the Hunter-Schmidt metaanaly- sis approach, this study contributes to the body of knowledge by quantifying the incon sistent findings of 39 studies that explore the relationship between SB and CSR activities and disclosure. Based on the analysis, the existence of IB and NED has been proven to significantly impact the effectiveness of dis- closing CSR. However, the effect of OD on CSR still varies. This meta-analysis study supports the assertions of agency theory, stakeholders’ theory, and legitimacy theory that corporate governance significantly influences the company’s activities and disclosure in society and the environment. The monitoring system provides adequate supervision to encourage the executive to concern the stakeholders and shareholders more equally.

On the other hand, not all parts of SB positively and significantly influence CSR. Based on the meta-study from 39 works of literatu re, OD has failed to improve CSR activities and disclosure. This meta-analysis offers a notable outcome in that the high quality of the publi cation provides evidence related to the relationship between SB the CSR and the impact in studies published in Scopus-listed journals.

Financing

This research did not receive a specific grant from any funding agency in the public, commercial, or nonprofit sectors

Conflict of Interest Statement

The authors declare no potential conflicts of interest concerning this article’s research, authorship, and publication.

Statement of Ethical Approval or Informed Consent

All information extracted from the study will be encrypted to protect the name of each subject. No names or other identifying information will be used when discussing or re- porting data. All subjects gave their informed consent for inclusion before participating in the study. The investigators will securely keep all collected files and data in a locked cabinet in the principal investigators’ office.